Unqualified Opinions 4/24/23 - 4/28/23

By Tim Hanson

Where Did the Money Come From? (4/24/23)

Emily (our MD) sent me this cautionary tale about a guy who won an auction for the famous (because it’s a triangle!) Flatiron Building in New York City and then couldn’t even produce his $19 million deposit. You would have thought somebody would have asked for proof of funds from any potential bidder beforehand because now a lot of work has been done and no one is any closer to closing a deal.

If you remember your risks, this is counterparty risk, or “the risk that the other side of the trade will fail to perform.” The obvious lesson is that before doing a deal, make sure the other side has the money.

But I also think counterparty risk is more than just black or white. You not only want to know if your counterparty has the money, but also where he/she/they got the money from. Because while the source of capital may not be what determines whether it’s there or not, it absolutely will determine how it behaves. And if you’re going to be stuck with your counterparty for any length of time after a transaction closes, that matters.

Here’s a hypothetical…

Let’s say you were Twitter. Would you have rather taken an investment from Warren Buffett or Elon Musk? If you don’t know what you know now about how Musk has run Twitter since his investment, I actually think the answer to this question is a pretty close call. Despite Buffett’s reputation, it’s unlikely he could have helped the company. He is typically hands-off and doesn’t cop to having much knowledge about technology whereas Musk is (was?) one of the foremost technologists on the planet.

And – hot take – I actually think Musk could have been (and may turn out to be) a pretty great owner of Twitter. What tripped him up was the fact that he overpaid for the company using high interest rate debt and personal wealth tied to leveraged, highly volatile stock. This is not high quality capital. Instead, it’s expensive and short-term and what has happened at Twitter since Musk’s investment – the cost cutting, aggressive monetization, etc. – is always what happens when a deal is closed using expensive, short-term capital. In other words, the root problem isn’t necessarily who provided the money but where the money came from.

We teach kids that it’s rude to ask anyone where they got their money from, but (1) it’s a really important question and (2) anyone who actually has high quality capital should be proud to tell you about it.

Apple Watch Psychopaths

(4/25/23)

Luckily, I live out in the country because otherwise I would be embarrassed by my neighbors seeing me sprint down my driveway at 9pm risking life and limb because my Apple Watch told me I could still do it and burn the 40 calories left to hit my Move goal.

Yes, I’m a psychopath. Does anyone else have this kind of dysfunctional relationship with their Apple Watch?

The answer has to be “Yes,” right? Because everybody has them. I look around now and see so many square faces on wrists despite the fact that it was viewed as a failed product upon its release. And it should have been, if it didn’t become so darn useful. Absent its judginess, it’s a no-brainer. That said, every day I think about going back to the Timex Ironman I keep in my bedside table.

But I digress…

Which brings us to metrics, which are both the most important and most dangerous concept to introduce to any business…or really any group of people. If you have them and you understand them and you work towards them, metrics can be unlocking and important. But if you try to achieve them at any cost without regard to nuance, they can be your undoing…fast. To bring this all full circle, yes, it’s frustrating to come up short of an arbitrary but well-intentioned goal, but do those last 40 calories really matter in the scheme of things and should I be out in the pitch black with a headlamp instead of helping put my kids to bed?

But I digress again…

When it comes to metrics, three things matter: (1) What; (2) When; and (3) How.

What is the variable you are measuring. Make sure these are items that matter and that are leading indicators i.e., predictive and not lagging indicators i.e., reactive.

When is the time period over which you are measuring your What. Does an hour matter? A day? A week? A month? A quarter? A year? Make sure what you are measuring is calibrated with when you are measuring it and that the two together provide meaningful information.

And finally How are you achieving the What over the When? As Mark notes, if you’re measuring a rate, make sure you’re also measuring a volume of throughput. And if you’re measuring volume, make sure you’re almost measuring a rate of quality. Moreover, ask if what you’re doing makes you proud? And is it sustainable or does it carry hidden costs i.e., does it make you want to go back to your Timex Ironman?

These are also important questions even if your What and your When are spot on.

People Who Worked For Me

(4/26/23)

There are inside jokes and there are inside jokes by which I mean jokes that are only funny to the person telling them and my relentless trolling of Morgan Housel for a retweet certainly falls into the latter category. (But it did make me laugh.)

If you don’t know Morgan, he is today a best-selling author, partner at the Collaborative Fund, and an in-demand speaker on behavioral finance (who we just happen to have a podcast conversation with out today). Plus, he’s a great dude. What’s also true is that at one point in a past life he worked for me.

Morgan’s always been a great writer, but he’s never been strong on change and he and I had a lot of conversations before he decided to move on to something next. That probably seemed like a net negative for the organization we both worked for at the time, but it turned out to be a great move for everyone involved. No one doesn’t benefit from others achieving great things. And now instead of managing him, I get to free ride on his 450 thousand followers.

Lesser-known than Morgan, but still great, is Michele Hansen (who has fewer Twitter followers than Morgan, but still more than me). She, too, worked for me in a past life while also founding and bootstrapping her own software company, Geocodio. She’s since gone on to run that company full-time while also finding time to write a book and host a podcast (Morgan has a new podcast too).

I’m plugging my friends and former direct reports here because I’m proud. I think the best measure of anyone is what the people you might be helpful to go on to do next. And while it’s insanely egotistical of me to believe I had anything to do with any of this, Morgan did send me an inscribed copy of The Psychology of Money that I keep on my desk and Michele did send me a Geocodio sticker that I put on my laptop because both inspire me and remind me when I see them of what matters when it comes to people.

Wait Until Something Really Bad Happens

(4/27/23)

After I wrote about the importance of having fun at work I received a note from Ellen Twomey, Managing Director of Fugitive Labs in Atlanta. She said the Opinion really hit home and that fun was a great benchmark.

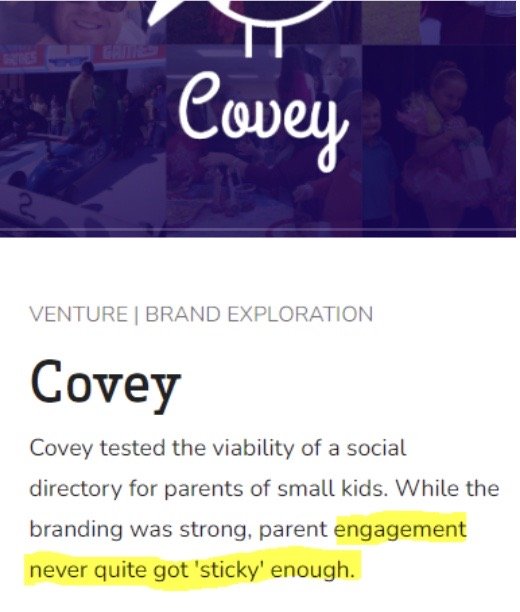

Intrigued, I looked up Fugitive Labs and it looks fun too!

But more interestingly I saw something on their website that I hadn’t seen before – a case study that featured a product of theirs that didn’t work…

I love that. No one bats one thousand and anyone who represents nothing but success is hiding something. Moreover, failing is important. Not only is it how we learn, but if you haven’t failed yet, failure is coming because you haven’t yet pushed the boundaries of what’s possible. And if you haven’t done that, it may mean that you don’t have enough experience.

For example, one of the common questions we got back when we were raising capital was “Can you tell me about an investment you made that hasn’t done well?” We all have those and we had one of those then as we do now and will in the future and so would tell people about what went wrong and what we were trying to do to make it right. Usually it would end then and we would move on to another topic.

But one of the more interesting reactions to our answer to that question was someone who said “Huh, that’s not that bad. Good for you. But we only invest in managers who have had something really, really, really bad happen to them.”

That struck me. On the one hand it was preposterous. Isn’t avoiding catastrophe a sign that you might be good at something? But on the other, there was logic to it. Perhaps the only way to avoid a catastrophe is to have already had one and therefore know what it looks like when one’s coming.

Either way, everyone fails at something eventually and I think the world would be a more interesting place if we were able to follow the lead of Fugitive Labs and put our failures front and center on our websites, resumes, and LinkedIn profiles.

Follow Simple Rules

(4/28/23)

After I wrote about walking the fine line between knowing everything and knowing what matters, I got a nice response from @MikeBotkin who runs a holdco out of Florida. He said that he and his partner had spent hours that same day debating the same topic and reached a similar conclusion that “it depends.”

And whereas I had tackled the topic from a risk management perspective, he’d been focused on operations and specifically what does he need to know about how one of his businesses is being run versus what he trusts his CEOs to know. Then he added something profound:

“From our viewpoint, there has to be so much room for a CEO to a) lead b) perform c) grow…and most importantly…d) mess up.”

What’s interesting about those four factors is that I don’t think you can do one of them without also ending up doing the other three, yet three of them are celebrated as positives while messing up is typically not. But let me be clear, you need to mess up in order to lead, perform,and grow.

Quick aside, I was having dinner recently with a family that had a family office in which their recently graduated son was starting as an equity analyst. Mom found out what I do for a living and asked me what advice I had for her son. “Make a bad investment,” I said (Mom was not amused).

In the past I’ve expressed a pessimistic view of regulation. And it was after one such missive that my buddy Nate sent me “The dog and the frisbee.”

Published in 2012 after the Great Financial Crisis, the paper explores the idea that complexity is to blame for watchdogs’ failure to prevent crises. The entire thing is worth the read (particularly if you enjoy the minutia of financial regulation), but the two ideas that most resonated with me were “the more complex the environment, the greater the perils of complex control” and that simple strategies in sports, medicine, investing, and more tend to outperform complicated ones.

As for what these things have to do with one another, it’s the idea that no matter how much you know, you cannot prevent the realization of risk. To wit, banks have to submit tens of thousands of data points to PhDs on a regular basis and yet several more just failed.

The takeaway is that in a complex and overengineered world, whether it comes to managing investment risk, banking regulations, or people who work for you, try to follow a small number of simple rules. They won’t always work, but hopefully it will be obvious when they don’t apply, or more importantly, when you’re breaking them.

Have a great weekend.

Want Unqualified Opinions delivered to your inbox every weekday?