Unqualified Opinions 3/27/23 - 3/31/23

By Tim Hanson

Why We Negotiate for Worthless Terms

(3/27/2023)

There I was, sitting at my desk, my HP laptop overheating as I tried to build a model in Excel that simulated 5,000 random 25-year sequences of events helping Caroline demonstrate to an outside independent auditor that a preferential term we had built into our equity at one of our investments wasn’t worth anything.

First, a note about auditors, regulators, or really anyone tasked with oversight. When they show up to examine you, they will find something wrong. That’s their job and people like to show the people they report to that they can do their job (mostly). So if you have that mindset going into one of these situations, you can leave a lot of frustration on the cutting room floor.

Back to my overheating laptop…

What I think the auditors were skeptical of is the fact that we had negotiated for a term that on its face wasn’t worth very much. In this case we’d been asked to pay a higher valuation than we normally would to make an investment. We wanted to do it – we liked the business, people, and opportunity – but we also didn’t want to get our asses handed to us because we overpaid. Remember, the only way to definitively lose a game is if it doesn’t end on your terms.

So we said to our prospective partners something like: Look, if reality is within spitting distance of plan, we’ll split everything pro rata, but if the bottom falls out, we get all of the earnings until the business recovers. And the only reason for that is that we’re investing at a valuation where we can’t hazard the risk of the bottom falling out and only get part of the economics.

Because we both believed there was a low probability of that happening, they said fine.

My Excel spreadsheet proved that assumption out. The median value of all of those randomizations was zero and the mean was immaterial. So there was a chance the preference could come into play, but it was indeed a small one.

So why did we negotiate for a “worthless” term? Because we never want the game to end.

Howard Schultz: 3x Starbucks CEO

(3/28/23)

Hulk Hogan is the best WWE champion ever. I agree. But then you have this nonsense where wrestlers like Brock Lesnar are aggrandized for being a 12-time world champion.

Being a 12-time world champion is great and all, but it also means you lost the championship and had to win it back 11 times.

Of course, professional wrestling outcomes are preordained, so who cares? But why is Howard Schultz the three-time CEO of Starbucks?

I met the second Howard Schultz replacement way back when, when the two of them came to speak at an event I attended and you could tell immediately he wouldn’t last long. His name was Jim Donald and he was from Pathmark (a low quality now mostly defunct chain of grocery stores in the Northeast) and the two just didn’t coalesce. This was 2005-ish and Schutlz re-replaced him by 2008. You could tell seeing them interact it wasn’t a long-term fit and when Schultz talked over Donald on investor conference calls it was awkward.

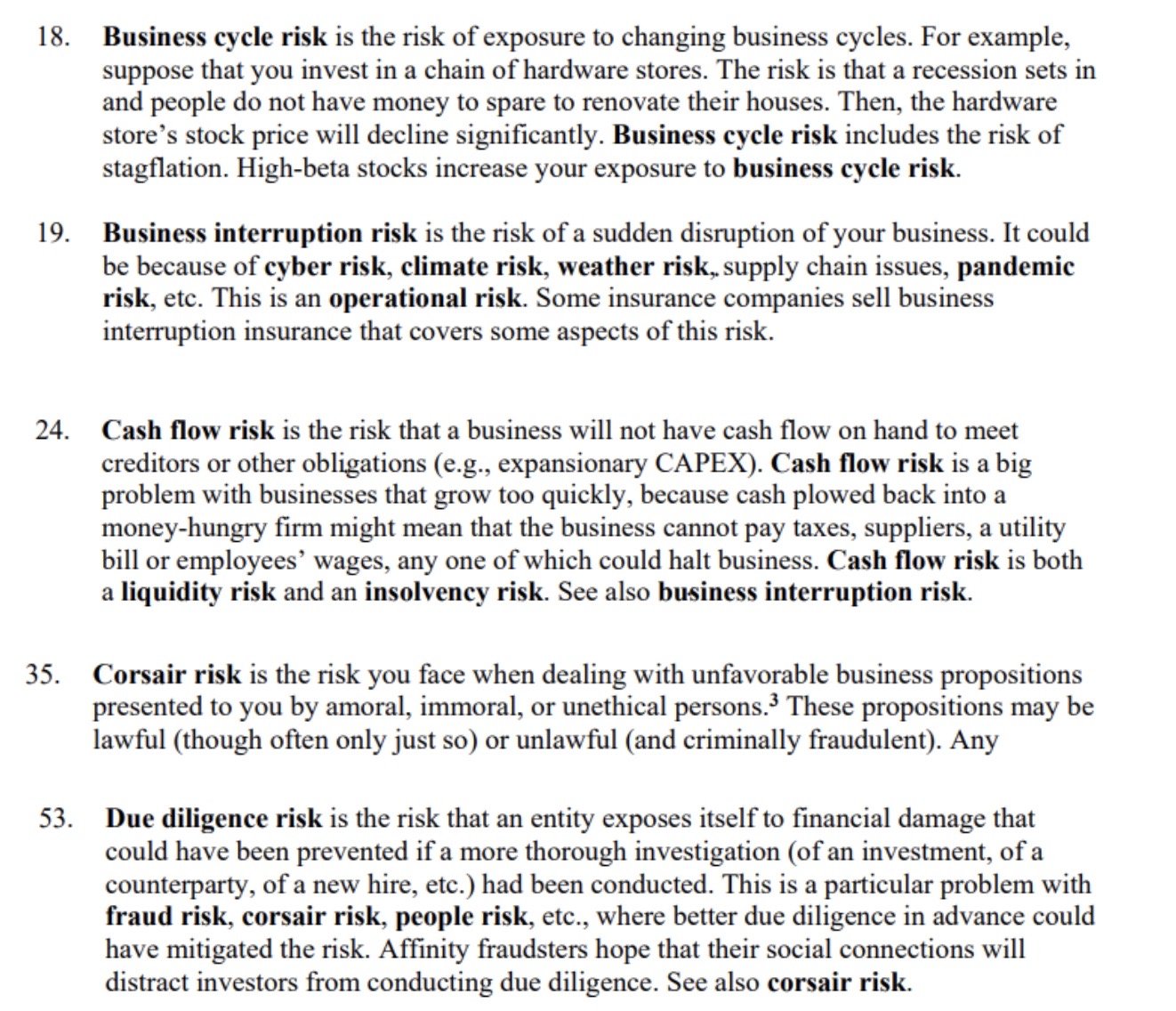

Schultz stayed in his second stint as CEO until 2017 but then stepped back in again in 2022 after the person who replaced him retired.

Now it’s 2023 and Schultz permanently retired last week with his fourth replacement having learned under his tutelage since September. We’ll see how it goes, but I suspect Starbucks hasn’t seen the last of Howard Schultz.

And maybe that’s a good thing. Here’s a long-term chart of Starbucks stock. I’ve highlighted the times when Howard Schultz was CEO.

The stock has mostly performed a lot better with him in charge. But this seems like a failure in transition planning, no?

A successful organization cannot be led by one and only one individual. Nor should an individual believe that he or she is the only one who can lead a specific organization. Because if that’s the case, it’s only a matter of time before the wheels come off.

If you’re a leader, the most valuable way you can spend your time is on training your replacement. Maybe Schultz knows this now and that’s why he’s spent the last seven months training newly minted Starbucks CEO Laxman Narasimhan. We shall see.

Zero Tolerance OR Materiality

(3/29/23)

Clayton (who runs Capital Camp) emailed me after I wrote about the fine line between having a zero tolerance policy towards errors versus focusing on material issues only. What, he asked, is a tolerable amount of slippage in a situation and what variables should go into making that case by case decision?

It’s a good question because there’s no good answer, but here are some considerations…

If you see a small problem, whether you address it or not probably depends on how fast it is likely to get worse and what the ultimate downside is when it does. In my previous example of small, questionable credit card charges turning into full-scale fraud if they’re not caught early, the rate of decay of the problem is exponential and the downside tremendous. Because when the thieves see that they can get away with something small, their next gambit is likely to max out the card, so zero tolerance applies.

But if a small problem is ring-fenced i.e., even if it does get bigger, it can't escape or become material, let it fester. This applies a lot in parenting where by letting a small problem persist, your kiddo usually learns how to solve it on their own terms. And does it really matter if yours is the one never wearing shoes?

A third way is to let a problem linger, but watch it like a hawk so you can intervene if it runs the risk of becoming material and spilling over. This is more time-consuming than either a zero tolerance or materiality approach, but you get some of the benefits of both. Of course, this approach can be dangerous in that it’s also egotistical. If you adopt it, it means that you think you will know the right time to step-in and be able to put something back on the rails which, you know, is the entire premise of Jurassic Park.

And a fourth is that you allow a problem to continue because you are deriving a benefit from it somewhere else and therefore are tolerating a material issue because the entire equation of variables nets to immateriality. A classic example of this is the employee that contributes greatly to the P&L and is a drag on culture…like a copywriter I once worked with who authored high ROI campaigns but also diminished the brand and berated coworkers. This one is difficult to manage because by solving the problem you are creating another problem. I think the tactic here is to celebrate the good but set benchmarks around the bad and cut bait if the negative side of the equation doesn’t show signs of improving.

But you need to decide for yourself what is and isn’t worth it.

Stolen Bases, Qwikster, and Changing the Game

(3/30/23)

It’s Opening Day, which means it’s as good a time as ever to point out that baseball curmudgeons today bemoan the decline of the stolen base. Once one of the more exciting parts of the game with league leaders like Rickey Henderson and Vince Coleman in the 1980s swiping upwards of 100 bags per season, the league leader in 2022, Jon Berti, stole just 41.

And that’s not because players are getting slower. In fact, players today are more likely than ever to steal a base when they try. The problem is that baseball teams have decided that stealing a base isn’t worth the risk. The player attempting a steal could be tagged out and saving that out is more valuable to the prospect of winning.

But count me as a curmudgeon who likes stolen bases. Where, other than in sports, can it be so much fun to take risk? So I sit around a lot and think about changes that might bring them back. Like what if baseball increased the value of stolen bases by letting teams backfill? In other words, if a player successfully steals second, the team gets to put another runner back on first. If a player steals third, they get to load the bases. And if he steals home, which for my money is one of the most exciting events in sports, it counts for four runs, the same as a grand slam.

Yes, that changes the fundamental rules of the game, but the fundamental rules of baseball were written when players weren’t quite in such good shape and did not know about optimizing for launch angles and other details that have enabled home runs to proliferate. What if the fundamentals are supposed to be that home runs are rare and stolen bases more common?

That’s tilting at windmills stuff because change is inevitable. But all of it is to say that if you want to change the trajectory of where something is heading, you may need to radically change the rules of engagement.

For example, Netflix got its start as a DVD-by-mail business. You used the internet to pick which movies you wanted to see, but then they were sent to you in red envelopes. Over time it became faster and more convenient to stream movies directly from the internet. This is a point where Netflix could have been disrupted. Rather than invest in the technology and content rights to make that possible, it could have tried to delay the inevitable and compete by paying to overnight all of its DVDs so they would get there faster or some such.

And in fact it did do something like that by splitting the company into two businesses: Netflix, which would spend on streaming, and Qwikster, which would try to preserve the legacy business. It was a "have your cake and eat it too" moment with CEO Reed Hastings writing at the time that “streaming and DVD by mail are becoming two quite different businesses, with very different cost structures…and we need to let each grow and operate independently.”

It didn’t work. Customers hated the idea of two subscriptions (there’s an adage in business that you should never let your customer see your business model and this was Netflix going full blown open kimono) and frankly Qwikster was a melting ice cube. Play it the other way and if Netflix had stuck to its DVD by mail guns and not changed the game, ceding streaming to Amazon and others, it probably would have disappeared within 24 to 36 months.

When presented with challenges, spend time thinking about specific solutions, but if they are just bandages or attempts to delay the inevitable, probably don’t pursue them. Instead, consider ways to change the game entirely. These ideas aren’t always practical or the most cost efficient, but sometimes they are what’s needed.

As for baseball, it’s put a lot of bandages on its business model recently, including rule changes this year that include bigger bases and a pitch clock. But its popularity continues to decline and who knows what happens next. If that can happen to America’s Pastime, is any market share safe?

Everything You Need to Know about Risk

(3/31/23)

It’s not often that an academic research paper makes you laugh out loud, but that’s exactly what happened when I found this Easter egg inside of 150 Risks in Finance: An Alphabetical List of Definitions and Examples:

They appear to have a good sense of humor at the University of Otago. But they also know their risks, so I recommend you keep that link on hand as a handy reference guide.

There are also some exercises at the end where they propose scenarios and invite you to identify the inherent risks. I had fun reading those and figured it might be worthwhile to apply the framework to what we do…

Scenario: You have the opportunity to acquire a majority stake in a small business run by its retiring founder who says the business is in great shape. What risks do you face?

Let’s take them alphabetically…

I’ll stop there, but you get the point. Why do we do what we do again? Have a great weekend.

Want Unqualified Opinions delivered to your inbox every weekday?